The market for AI executive talent has changed faster than most compensation committees anticipated. Internal salary bands built on general engineering surveys are now routinely below market for senior AI roles, and the gap is widening. Organizations that rely on prior-year benchmarks to set offers for AI-native leaders are losing candidates to competitors who have already recalibrated.

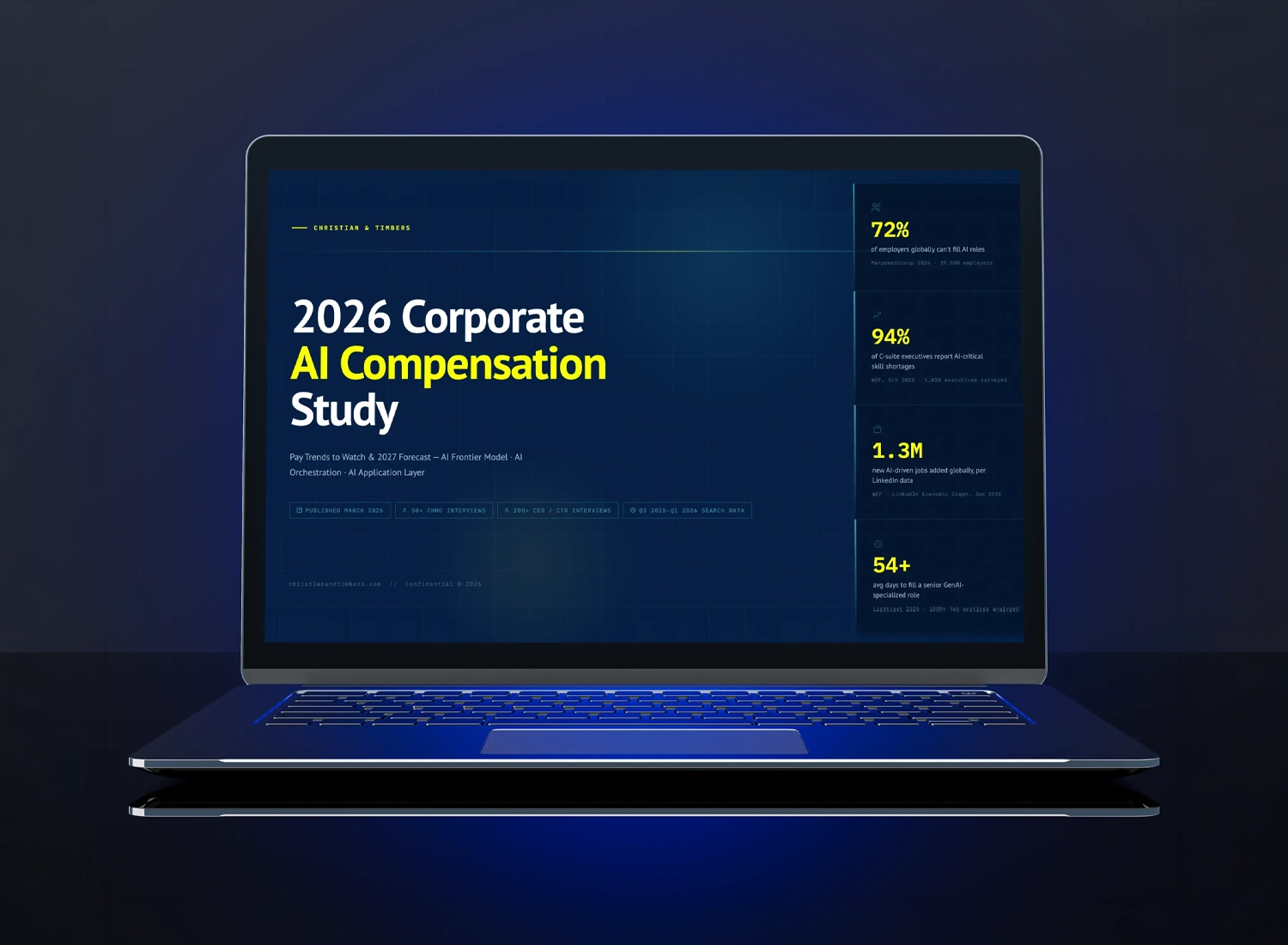

This article draws on the Christian & Timbers 2026 Corporate AI Compensation Study, which is based on proprietary closed-offer data spanning Q3 2025 through Q1 2026 and cross-referenced with data from Equilar, WTW, Ravio, Lightcast, ManpowerGroup, and the World Economic Forum. The result is a detailed picture of what AI executive compensation looks like right now and where it is heading in 2027.

If you are responsible for AI leadership hiring, retention, or board-level compensation decisions, the numbers in this article are directly relevant to your work.

Check the full compensation benchmarks here

The Market Conditions Driving This Shift

Three forces are simultaneously reshaping AI executive compensation: accelerating demand, collapsing supply, and structural changes in how companies design AI leadership roles.

On the demand side, AI/ML hiring grew 88% year over year in 2025, according to the Ravio 2026 Compensation Trends Report. That growth is not evenly distributed across job types. Entry-level tech hiring fell 73% in the same period, which means organizations are concentrating headcount investment at the senior and executive level. Companies are not building large AI teams from the ground up; they are hiring fewer, more senior people and expecting faster output.

On the supply side, ManpowerGroup's 2026 Talent Shortage Survey, based on responses from 39,000 employers across 41 countries, found that 72% report difficulty filling AI roles. For the first time in the history of that survey, AI skills have surpassed all other categories as the most difficult to source globally. Christian & Timbers' own search data, drawn from structured interviews with more than 50 CHROs and VPs of Talent and more than 200 CEOs, CTOs, CPOs, and board members, confirms this pattern. The average time to fill a senior GenAI-specialized role is 54 days, according to Lightcast data.

The structural change is the one most organizations are slowest to address. The role of the senior technology and AI executive has been redefined. The leaders organizations need in 2026 are not traditional CTOs with AI awareness bolted on. They are AI-native executives who take direct accountability for driving ROI across technology and AI initiatives, often across the entire organization. Ford's new CTO is leading the integration of AI into physical systems manufacturing operations. PepsiCo's Chief Digital Officer is overseeing AI transformation across supply chains and customer engagement. BP has appointed an AI-focused CTO to optimize operations and reduce emissions. These are not technology roles with exposure to AI. They are AI leadership roles with organizational authority.

That redefinition has a direct effect on compensation. When the scope of a role expands, the market price for that role expands with it.

What AI Roles Now Command in Base Salary

Christian & Timbers benchmarks AI executive compensation across five public company size bands, from organizations with 2,000 employees to those with 100,000 or more. The data covers 10 AI leadership and engineering titles, including roles that did not formally exist in prior compensation surveys: the AI-Native CTO, the AI-Native CIO, and the Chief Digital and Data Officer.

Across all size bands, AI roles carry a 67% salary premium over traditional software engineering roles, according to the Lightcast 2025 report and JobsPikr AI Salary Benchmark 2026. That premium is not a temporary artifact of a hot market. It reflects a genuine and persistent scarcity of leaders who combine technical depth in AI systems with the organizational authority to deploy them at scale.

At mid-size public companies, base salaries for AI-native executives in the 25th to 75th percentile range are materially higher than what most compensation committees have modeled. At the largest public companies, the gap between internal pay bands and actual market rates is even wider, in part because large organizations have been slower to revise their benchmarking methodology.

Mercer's 2026 US Compensation Planning Survey revealed that 83% of US employers still allocate salary budget increases evenly across the organization instead of focusing on high-demand skill areas. For AI leadership roles, that approach results in offers that are structurally below market value before negotiations even start.

Equity Structures Have Changed

Base salary is only part of the picture. Equity compensation at AI companies rose 25% in 2025 compared to 2024, according to Sequoia Capital's 2025 Total Compensation and Benefits Benchmark Report, which drew from 1,976 companies across 16 countries and more than 150,000 employees. That same report found that AI companies delivered the largest salary increases of any industry in 2024.

The structure of equity packages has also evolved. At VC-backed, PE-backed, and public companies, equity behaves differently by company stage and ownership model. Public company equity for AI executives in 2026 increasingly reflects retention priorities: longer vesting schedules, larger refresh grants, and front-loaded structures designed to close the gap between what a candidate holds in unvested equity at their current employer and what they would walk away from to take a new role.

Christian & Timbers' research tracks annualized equity ranges by title and company size band. For CHROs, CFOs, and compensation committees setting offer parameters, annualized equity is the figure that matters most for comparison purposes. A large one-time grant looks attractive in absolute terms, but it understates the annual cost of competing for this talent on a sustained basis.

Sign-on awards add another layer. In a market where candidates regularly hold significant unvested equity, sign-on grants have become a standard tool to cover the cost of departing from a prior employer. Organizations that do not budget for sign-on awards at the executive AI level are entering negotiations at a structural disadvantage.

The Titles That Define AI Leadership in 2026

One of the more significant findings in the Christian & Timbers 2026 study is the formalization of titles that did not appear in compensation surveys three years ago. The AI-Native CTO is now a distinct role from the traditional CTO, with a different scope, different reporting relationships in some organizations, and different market compensation. The same applies to the AI-Native CIO and the Chief Digital and Data Officer.

These titles reflect a genuine organizational shift. Companies are no longer asking whether their existing technology leadership is AI-aware. They are asking whether their technology leadership was built for an AI-native operating model. The answer, in most cases, is no, which is why executive search for these roles has accelerated and why compensation for candidates who fit the profile has increased sharply.

Christian & Timbers benchmarks all ten of these roles by title, company size, and component, including base salary, target bonus, and annualized equity. For boards and compensation committees, the value of role-specific benchmarks over general technology executive surveys is significant. Aggregated data understates the premium commanded by AI-native roles precisely because it includes traditional technology roles that do not carry the same market premium.

What the C-Suite Is Saying About AI Talent

The Data from structured interviews conducted by Christian & Timbers between Q3 2025 and Q1 2026 is consistent on one point: the C-suite understands that AI talent is scarce, but most organizations have not yet changed their compensation infrastructure to reflect that scarcity.

94% of C-suite executives surveyed report AI-critical skill shortages. That figure comes from WEF data and is consistent with what Christian & Timbers see in active search engagements. Organizations know that talent is hard to find. The disconnect is between that awareness and the internal processes, including compensation band approvals, equity budget allocations, and offer authorization timelines, that govern what they are actually able to put on the table.

In a search process in which the average time to fill a senior GenAI-specialized role is 54 days, delays in offer construction pose a material risk. Candidates at this level are typically in multiple processes simultaneously. An organization that takes three weeks to build an offer after identifying the right candidate is not operating at the pace the market requires.

The 1.3 million new AI-driven jobs added globally in 2025, per LinkedIn Economics and WEF data, represent a significant expansion of the competitive pool for senior AI talent. More roles competing for the same supply mean that compensation outcomes for candidates with the right profile will continue to rise.

How to Use Benchmark Data in Compensation Committee Decisions

For boards and compensation committees at public companies, the 2026 AI compensation environment creates specific governance responsibilities. Equity compensation for AI executives now falls outside the ranges established by prior benchmarking cycles. Committees that rely on data from 2024 or early 2025 surveys are working with figures that are no longer accurate.

Christian & Timbers' study is structured specifically for board-level use. The data is organized by company-size band, allowing committees at organizations with 2,000 employees to use the same framework as those at organizations with 100,000 or more, without averaging across a range that renders the benchmarks meaningless.

The WTW 2026 Global Pay Planning Report, drawn from 36,960 companies across 156 countries, documents that salary budgets are being reallocated toward AI-critical roles in organizations that have recognized the structural nature of the talent shortage. For boards, the question is not whether AI leadership compensation requires a separate framework. The question is how quickly that framework gets formalized.

Compensation committees that act now have an advantage. The organizations that standardize their AI executive compensation benchmarking process in 2026 will be better positioned for the retention cycles that follow, as equity grants vest and candidates become available to compete for roles.

What CHROs Need to Adjust Right Now

For CHROs and VPs of Talent, the immediate priority is to recalibrate the salary bands for senior AI positions. The Mercer finding that 83% of US employers still distribute salary budget increases equally across the organization is a useful diagnostic. If your organization applies uniform percentage increases to engineering and AI roles alike, your AI compensation bands are almost certainly below market.

The recalibration process requires role-specific data, not general technology surveys. Christian & Timbers' benchmark data covers the titles that appear in active AI executive searches and the company sizes where public company compensation decisions are made, with components broken out to allow direct comparison to current offer activity.

Beyond base salary, CHROs need to assess whether their equity authorization processes are fast enough to keep pace with the market. An offer that takes three weeks to clear internal approval frequently does not close. The speed of offer construction is itself a competitive variable in AI executive search.

The interview data Christian & Timbers collected from more than 50 CHROs also points to a recurring challenge with internal equity. When organizations bring in AI-native executives at market rates, those rates often exceed what current senior technology leaders earn. Managing that compression requires a proactive approach to retention compensation for existing leaders, not just new offer construction.

Looking Ahead: 2027 Compensation Forecasts

The Christian & Timbers 2026 study includes role-by-role compensation forecasts through 2027. The directional signal is consistent: AI executive compensation will continue to rise, and the pace of that increase will outrun general executive compensation inflation.

The factors driving that forecast are structural. The supply of AI-native executives who have led organizations through full AI transformation cycles at scale remains limited. The number of public companies actively competing for that talent is growing. The consequence is that premium candidates will continue to command premium offers, and the definition of premium will shift upward.

For organizations planning 2027 hiring or retention cycles, the 2026 benchmark data is a starting point, not a ceiling. Building offer models assuming 2026 rates will hold through 2027 is a planning risk.

Access the Full Compensation Benchmarks

The Christian & Timbers 2026 Corporate AI Compensation Study includes complete benchmark data for all 10 AI leadership and engineering titles across 5 public-company size bands. The study was designed for CHROs, CFOs, CEOs, and board compensation committees at public companies, who make AI leadership hiring and retention decisions.

Check the full compensation benchmarks here