Advisory roles are experiencing a quiet resurgence in PE-backed companies for a simple reason: the cost of being late has risen. Being late to a category shift, an enterprise buying motion, a regulatory posture, or an operational inflection that investors can already see in the numbers comes with higher stakes.

When the right advisor is structured correctly, the relationship shortens the time needed to achieve results. It sends strong signals to executives, speeds up hiring, sharpens product development and go-to-market strategies, and enhances credibility with customers and partners who assess leadership quality before considering features. Conversely, when the structure is flawed, advisory equity becomes an expensive line item with weak accountability, unclear deliverables, and governance risks that are awkward to manage.

Christian & Timbers Executive Search compiled benchmark data on equity compensation for advisory roles in publicly traded or high-profile companies. The following data provides PE sponsors, CEOs, CFOs, and compensation leaders with a disciplined benchmark for advisory equity in both upper mid-market and upper-market contexts.

What the benchmark actually measures

These benchmarks reflect equity value granted for advisory roles over a four-year period, based on observed market behavior in organizations of similar scale and profile.

This is not a universal pricing grid for every startup. It is a decision support framework for companies where:

- the cap table matters

- governance expectations are formal

- investor scrutiny is high

- advisory relationships must be defensible to boards and ICs

The two bands that matter

Most teams discuss advisory equity as if it were a single spectrum. In practice, the market splits into two ranges that behave differently.

1) Full market range that includes marquee advisors

For organizations of the size and scale referenced, equity grants generally range from $200,000 to $1,000,000 over four years.

This range includes the headline names, the former CEOs, the category icons, and the profiles who shift perception before they speak.

2) The typical band for strong advisors when you exclude the marquee premium

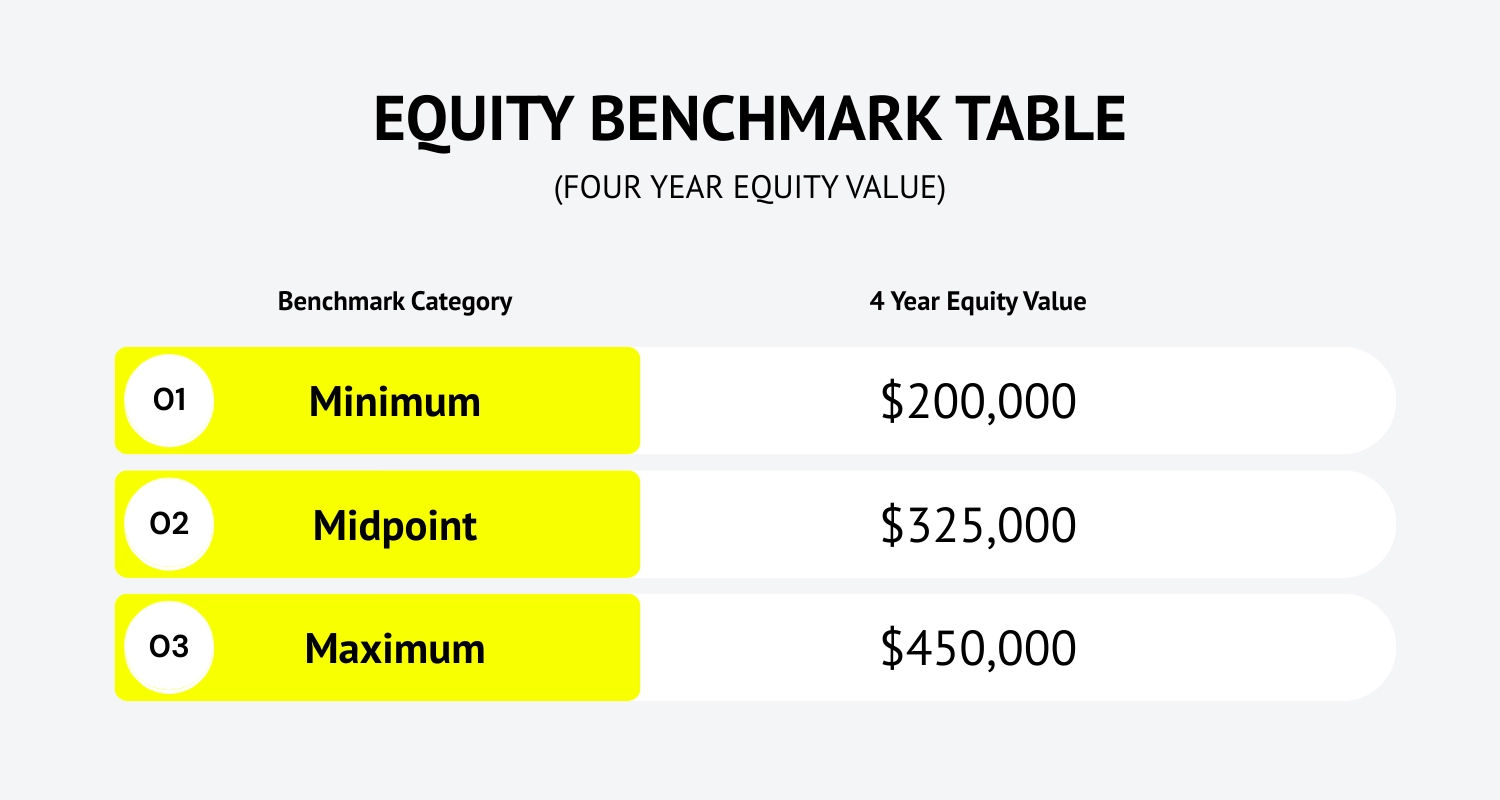

When excluding the highest visibility advisors, the typical equity band observed at similarly sized companies is $200,000 to $450,000 over four years.

This is the real working range for most advisory engagements that deliver meaningful value without requiring public market famous credentials.

Why this benchmark matters for PE-backed companies

The PE environment rewards clarity. Advisory equity has to survive three filters:

- Investment committee logic - Does the equity correlate to a value creation lever the sponsor already believes in, or is it a prestige spend.

- Board governance - Is the advisor accountable? Is the scope documented? Are conflicts managed? Is confidentiality tight.

- Management operating reality - Does the advisor improve outcomes, or add meetings and ambiguity?

Benchmarks reduce guesswork. They also reduce internal friction. When CFO, CEO, and sponsor share the same market anchor, negotiations become about scope and impact rather than ego.

The advisory equity decision framework boards actually respect

Equity is not payment. It is alignment. The strongest advisory engagements treat equity as an instrument tied to explicit value drivers.

Here is a practical framework that consistently produces board-level clarity.

Step 1. Define the advisory archetype in one sentence

Most advisory scopes fail because they are written as biographies rather than business mandates.

Use a single sentence that contains:

- the outcome

- the domain

- the time horizon

Examples of clean scope language:

- Enterprise credibility and deal acceleration for Fortune 500 procurement buying motions over the next 12 months

- Product strategy and pricing architecture for an AI-enabled platform shifting from SMB to mid-market over the next two quarters

- Regulatory posture and risk governance for an expansion into a highly regulated sector over the next 18 months

If you cannot write that sentence, the equity conversation is premature.

Step 2. Identify the value creation lever the advisor is attached to

Advisors have different value creation mechanics. The equity should reflect which mechanic you are buying.

Common levers in PE-backed environments:

- accelerating revenue through trusted executive access and deal de-risk

- compressing product cycle time through design decisions that prevent expensive rewrites

- strengthening operational resilience through proven playbooks that reduce burn and execution volatility

- improving talent density through network-based recruitment at the top of the org chart

- elevating governance in risk-sensitive sectors to protect exits and strategic optionality

When the lever is vague, equity drifts upward because value cannot be argued downward.

Step 3. Translate accountability into cadence and deliverables

Boards do not dislike advisors. They dislike ambiguity.

High signal advisory contracts usually include:

- defined cadence, for example, two calls per month plus ad hoc support during critical cycles

- deliverables, such as a go-to-market blueprint, partner map, hiring slate inputs, or decision memos

- stakeholder map, clarifying CEO and sponsor touchpoints, plus boundaries for management team access

- conflict and confidentiality terms that reflect the company’s enterprise maturity

This is where fragile advisory engagements become credible.

Where the money tends to land and why

The benchmark range tells you where the market is. The more useful question is how companies end up in one part of the range versus another.

The $200,000 to $450,000 band

This is typical when the advisor is:

- materially helpful

- not a public figure

- scoped to a specific operating mandate

- engaged with measurable cadence

In this band, the company is buying precision. The advisor is a lever, not a logo.

The $500,000 to $1,000,000 band

This band is typically reserved for advisors who create economic impact through visibility and trust transfer. The premium is often justified when:

- their name changes enterprise conversations before the product is fully mature

- they unlock partnerships that shift distribution

- they materially accelerate leadership hiring through their credibility

- they de-risk the story for future capital or an exit process

Premium grants need premium logic. Without that logic, equity at this level looks like a governance error.

Structuring the equity so it aligns with outcomes

The benchmark is framed as a year equity value. Modeling the equity value is only step one. How you grant and vest matters just as much.

Common structuring principles that fit PE-backed governance:

1) Time alignment

Advisors typically deliver value early. The structure should reflect the real arc of impact rather than defaulting to a generic pattern.

2) Milestones where it makes sense

For advisors tied to a discrete business outcome, milestone vesting can create sharper alignment. It also gives the board a cleaner rationale for the grant.

3) Clean optics with future stakeholders

Future strategic buyers and later-stage investors examine governance. Advisory equity with unclear scope can show up as a red flag during diligence. Tight documentation protects the company.

Common failure modes and how to avoid them

Even sophisticated teams repeat the same mistakes.

Failure mode 1. Paying for proximity rather than impact

Some advisors look impressive but deliver soft value. Fix this through scope discipline and deliverables.

Failure mode 2. Treating advisory equity like a substitute for hiring

If the company needs an operator, an advisor will not solve the problem. Advisory equity should not be a cheaper alternative to leadership.

Failure mode 3. Ignoring conflicts until you have one

High-profile advisors often have multiple relationships. Conflict clarity should exist before the first meeting, not after the first sensitive conversation.

Failure mode 4. Letting the negotiation be driven by the advisor’s prior package

Prior packages are context, not guidance. Scope and leverage should be the primary drivers. Benchmarks keep you anchored when the conversation becomes anecdote heavy.

Language you can use internally to align stakeholders

If you need a crisp internal narrative for sponsor, CEO, and comp leadership alignment, use this:

- The benchmark for advisory equity in companies of this scale typically sits at $200,000 to $450,000 over four years.

- We reserve $500,000 to $1,000,000 outcomes for marquee profiles where visibility and credibility transfer create measurable economic upside.

- Our proposed grant maps to a defined value creation lever, with clear cadence, deliverables, and governance guardrails.

It reads like a policy because it is one.

Practical takeaway for upper mid-market and upper market teams

This benchmark gives you a disciplined starting point.

- Use $200,000 to $450,000 over four years as the working band for most advisory roles.

- Move above that band only when the advisor’s visibility and credibility transfer create a measurable acceleration in revenue, partnerships, financing optionality, or leadership hiring.

- Document scope, cadence, and conflicts with board-level clarity.